Investing

in Cyclical Businesses

And

Braemar Shipping PLC

Economic cycle, courtesy Wikipedia

All businesses are influenced by the economic/business/stock-market

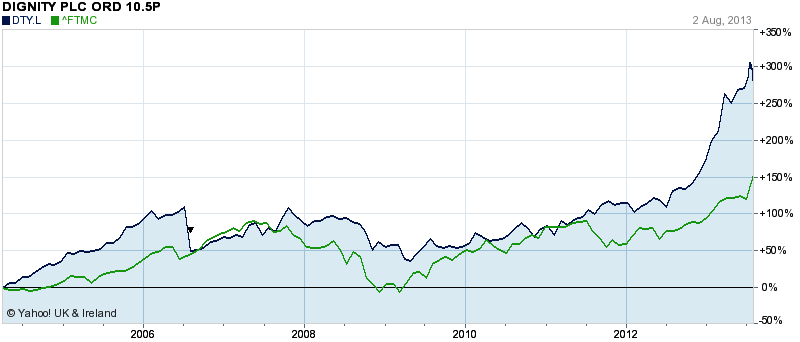

cycle. Consider Dignity PLC, the UK quoted funeral service company. In

its 2004 Annual Report, Dignity predicted its market for 2005:

"Historically,

fluctuations in recorded deaths have tended to be self-correcting and the

Board’s view on death rates continues to rely on government forecasts. Based on

these forecasts, we expect 579,700 deaths in 2005."

The actual number of deaths in the UK in 2005 was 582,639. No other

business I know can forecast demand a year in advance with 99.5% accuracy. And,

from one year to the next, the number of deaths never varies by more than about

5%. Yet Dignity's share price (in blue) has fluctuated with the

movements in the FTSE 250 (in green).

Graph courtesy of Yahoo, click to

enlarge

Opposed to industries like Dignity's, what are normally considered

cyclical industries - property, house building, engineering, mining, banking,

shipping etcetera - present a difficulty for the long-term investor. Their

irregular earnings, coupled with the threat of bankruptcies, ruinous 'schemes

of arrangement' or desperately priced rights issues at the cycle's bottom, make

them hard to value. The FTSE All-Engineer Index (in blue) compared to the

Gas and Water Utility index (in green) illustrates the opportunity of investing

in cyclical businesses:

Courtesy Yahoo, click to enlarge

And the FTSE Banks Index (in blue) compared to the same Gas and

Water Utility Index (in green) illustrates the risks:

Courtesy Yahoo, click to enlarge

Long-term investors will prefer the steadier income streams from

non-cyclical industries - utilities, food, personal

care, healthcare etcetera (see companies valued in previous posts). And from

those companies that have established a private market among consumers and/or

professionals; these include the online and catalogue clothing retailer N

Brown, the accounting software provider Sage, the education

materials provider and financial publisher Pearson and British Sky

Broadcasting, all valued in previous articles on this blog.

But there are times, and now is one, when many non-cyclical

industries are valued too highly by the stock market. For instance, the funeral

services company Dignity, at 1500p a share, is priced on a multiple of

22 times earnings and yields a scanty 1.1%. The long-term investor can sit on

his or her cash or venture into cyclical companies.

The cautious investor will want to:

1. Assess whether the cyclical industry is growing or not

from one cycle to the next.

2. Understand what the causes of the cycle are. It helps to

quantify the most relevant factors. Cyclical companies often refer to industry

standard statistics when presenting their results.

3. Know at what point of the cycle the industry is in now.

Timing is very important. Industry sources (trade journals, company news and

reports) help.

4. Be prepared to sell when there is evidence the cycle has

entered the boom phase. Here a target price and a stop loss are most useful.

---------------------------------------------------------------------------------------------------

Braemar

Shipping Services PLC

Unloading at port of Mumbai, India,

courtesy Wikipedia

Shipping volumes depend on international trade, and international

trade grows - and falls - at about twice the rate of world GDP. Since 2000, merchandise exports have grown at a cumulative 5% per

annum. This includes the 19% fall that occurred during the financial crisis.

Since then, merchandise exports have been growing at over 9% p.a.

Graph courtesy of Wikipedia, click to

enlarge

While trade and shipping volumes have recovered, shipping rates have

not. The standard measure for shipping rates that

exclude oil and containers, the Baltic Dry Index*, recently shows the

most alarming volatility:

Graph courtesy of Wikipedia, click to

enlarge

*The Baltic Dry Index

provides an assessment of the price of moving the major raw materials by sea.

Taking in 23 shipping routes measured on a time-charter basis, the index covers

dry bulk carriers carrying a range

of commodities including coal, iron ore and grain.

The Harper-Peterson Index for transporting

containers and the Baltic Dirty Tanker Index for transporting oil also

boomed in the years preceding the financial crisis. Prices have yet to recover.

Ship owners ordered too many ships in the boom years preceding 2009 and, as two

years pass between order and delivery, ships were still coming onto the market

when international trade had crashed. Fleets are young and it will take years

for shipping rates to recover.

However, shipping volumes continue to increase and shipbrokers that

provide services for shipping have benefited. Braemar Shipping Services

(BMS) is one. Braemar's share price (in blue) is more volatile than

the FTSE Small Cap Index (in green) to which it pertains:

Graph courtesy Yahoo, click to

enlarge

But Braemar's earnings and dividends are more stable than one would

expect from the above chart or from the volatility in shipping prices:

Braemar

|

2004

|

2005

|

2006

|

2007

|

2008

|

2009

|

2010

|

2011

|

2012

|

2013

|

Earnings

Per

share pence

|

14

|

29

|

36

|

32

|

49

|

56

|

47

|

47

|

33

|

32

|

Dividend

Per

share pence

|

13

|

16

|

18

|

19

|

23

|

24

|

25

|

26

|

26

|

26

|

Braemar is in good financial health.

Consider:

1. The company has held net cash for every one of the last 10

years. At February 2013, net cash, at 23 million pounds, was almost a

quarter of Braemar's market capitalization of 95 million pounds.

2. The balance sheet is clean of pension scheme liabilities. Braemar

only offers a defined contribution pension scheme to its employees.

3. Operating cash flow

(after deducting capital expenditure) of 40 million pounds these last 5 years

covered the dividend 1.6 times. Braemar has built up its newer businesses

through acquisition.

4. Return on equity for the last 3 years has averaged 12%.

In Braemar's 2013 Annual Report, management expect continued decline

from ship broking, an improvement in the technical and logistics business and a

decline in environmental during 2103/14. There are

no broker forecasts for this small company.

Braemar's nearest London-quoted competitor in ship broking and

services is Clarkson PLC, a constituent of the FTSE

250 Midcap. As such, Clarkson attracts the interest of analysts. Braemar

and Clarkson have a similar recent trading history, but Clarkson's

shares (at 1900p) are rated much more highly than Braemar's (at 458p):

P/E

Ratio

|

Dividend

yield

|

Price:Book

ratio

|

Net

cash as % market value

|

|

Braemar

|

14

|

5.8%

|

1.35

|

24%

|

Clarkson

|

22

|

2.7%

|

2.84

|

32%

|

Compared to Clarkson, Braemar looks to be good value at its current

price of 455p. But the investor will want to consider the following:

1. Braemar's main business continues to be ship broking,

which is still in recession.

2. While shipping volumes are increasing, there is still an

excess of ships of all kinds and there is no sign that rates are recovering.

3. When it comes, the increase in shipping rates, as measured by the

Baltic Dry Index, is likely to be sudden. And this will be reflected in

Braemar's share price.

4. As the stock market anticipates cyclical recoveries, the

investor is seemingly left with the option of buying in early, in the hope of

anticipating the market anticipating the recovery. The risk is that the cycle

has not reached bottom.

It is recommend to check dividend data of companies before buying stocks of any company. You need to have a brief look towards company data such as P/E ratio, dividend yield and net dividend offering in last 5 years. You can get all these data from any trust-able dividend online source. You can get all dividend news from UK dividend history.

ReplyDelete