Warren

Buffett

And

is Berkshire Hathaway Good Value?

Warren Buffett

in 2005 (Wikipedia)

There is something very comforting about Mr Buffett. Unlike that

geek Bill Gates or that wunderkind showman, the late Steve Jobs, Warren Buffett

seems like one of us. He is reputed to work from his study at the home he

bought in 1958 and to drive an old car. He lives in one of those vast, empty states

in America - Nebraska - where nothing ever happens, and he is addicted to one

of those fizzy, sugary American drinks, Cherry Coke. We can imagine him

flipping burgers at the barbecue and playing bridge with his chums.

But, as an investor, Mr Buffett is nothing like us. Son of a

stockbroker, he was a child prodigy investor and businessman. He studied

finance at Wharton and Columbia and worked with Benjamin Graham on Wall Street.

He is adept at using other people's money. At first the money came from his

partners - he provided the sweat and brains. Then, as CEO of Berkshire

Hathaway, he ventured into insurance because customers paid up in advance,

sometimes years in advance of their claims, and meanwhile he had use of their

funds for free. With the enormous funds at his disposal and a reputation for

integrity, he can make investments that we can only dream about.

What can we learn as investors from Mr Buffett? In his public

statements, company reports and annual letters to Berkshire shareholders

(available online at the company's website) he offers us his homespun

philosophy. It is couched in language as distant from the financial

gobbledegook of academics and financiers as Omaha is from Wall Street. But it

makes sense.

ü Invest only in what you understand.

ü Ignore the ups and downs of the stock market.

ü When everyone is predicting doom and stocks are

crashing at a stomach-churning rate, this is the best moment to buy.

ü When everyone is saying this is the moment to

buy and the stock market is in a state of euphoria, this is the worst moment to

buy and the best time to sell.

ü Instead of hiding from your mistakes, study

them carefully so you don't repeat them.

ü Buy for the long term, and as if you are about

to own the whole company.

Mr Buffett once said, "I'm 15 percent Fisher and 85 percent Benjamin Graham."

Phillip Fisher is the author of Common Stocks and Uncommon Profits, while

Graham is the author of The Intelligent Investor and, with Dodd, Security

Analysis. From Buffettology and other books written by third parties

on how he (supposedly) works, and from reading Fisher and Graham, one can get

an idea of his method.

Although everyone must come to his or her own conclusions, I would

start by asking these questions of any company (from Buffettology by

Mary Buffett).

- Do you understand the business?

- Is it a commodity business or is it not?

Does it have a ‘toll bridge’ or some class of monopoly? This is related to

ease of entry and the competitive position of the company.

- Does it have strong earnings that you can

forecast with a degree of certainty?

- Is it conservatively financed?

- Does it have a high return on equity?

- Does it retain earnings?

- Does it have low maintenance – i.e. low capital

expenditure and R & D?

- Does it have a good record of reinvesting

cash that it generates – via share buybacks, new ventures, acquisitions or

expanding the business?

- Can it adjust prices to inflation?

Once a company has been

identified as a suitable investment, what is its intrinsic value, and what

should one pay for a share? Finding the intrinsic value of a company is searching

for the Holy Grail, but there are techniques that can help. They will depend on

the nature of the business, but if it is a trading company one can use a simple

mathematical model that is centred on equity per share, earnings per share and

return on equity. As the quality of forecasts drops dramatically as time

proceeds, it seems wise to limit the necessary forecasting to 5 or at most 10

years. What will the company's share be worth then?

Benjamin Graham banged

home the concept of a margin of safety. For every investment he made an

evaluation of its intrinsic value and then allowed a margin of safety. Buffett

does the same.

A margin of safety can

be incorporated into the discount rate applied to the future value of the

share. The discount rate includes the cost of debt to the company plus a profit

plus the risk, or margin of safety. Discounting back the future value of the

share gives an approximate intrinsic value. We do not buy a share in the

company unless its market price is below our calculated intrinsic value.

Warren Buffett has

pledged nearly his entire fortune to charity.

--------------------------------------------------------------------------------------------------------

Is

Berkshire Hathaway Good Value?

Berkshire Hathaway is a conglomerate of businesses thrown together by two gentlemen

who are now in their eighties. It very obviously has a succession 'challenge'.

No one can replace Warren Buffett (and his partner Charlie Munger). He is the

patrician, the eminence gris, the company personified, the master

investor and he controls 34% of Berkshire's voting rights. As open as

ever, he discusses his succession plans at some depth in Berkshire's

2011 Annual Report (p. 97).

Buffett has gathered,

motivated and rewarded an extraordinarily talented group of people, who manage Berkshire's seventy plus concerns. This is,

perhaps, his greatest contribution to the company, and one has to wonder what

will happen to them when he retires (or dies in office). Will they all be happy

with the new chief? Will the new chief be able to keep them and motivate them?

Or will there be a stream of desertions, as they are lured away by companies

that can offer them the prize of running their own concern, without

interference from above?

A significant part of

Berkshire's growth has come via acquisitions. Owners

trust Buffett to keep their companies for ever in the Berkshire family.

This means that Buffett will hold on to underperforming businesses

indefinitely, but in exchange he gets first pick of the businesses for sale.

Will a new CEO be as patient? Or will he (the candidates are all men) reorganise

the empire by disposing of these underperforming assets?

The following graph

(Thompson-Reuters - click it to enlarge) is the embodiment of the Buffett

legend. Berkshire (blue) has vastly outperformed the S&P 500 (red)

since 1990, though the S & P 500 excludes reinvested dividends - and Berkshire

doesn't pay dividends.

Putting aside the

succession issue, is Berkshire good value now?

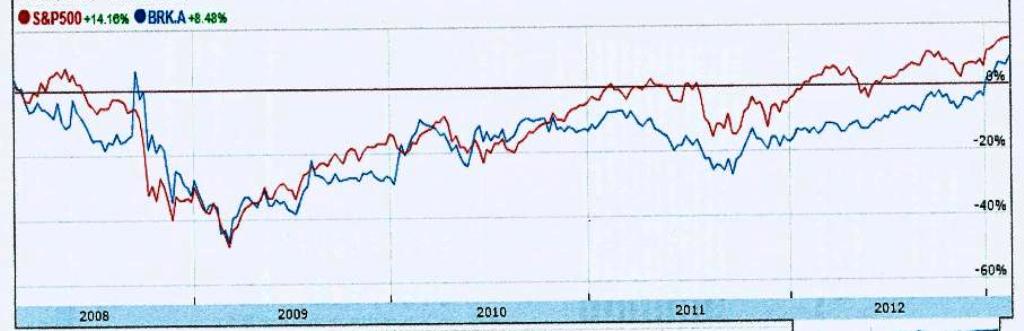

The past 5 turbulent

years have not been a happy time for Berkshire shareholders. They have

seen their stock appreciate by 8% while the S & P 500 has increased by 14%

or by about 30% with dividends reinvested. (Thompson-Reuters - click on the

graph to enlarge it)

What has happened? Berkshire's book value has increased by a

healthy 58% during this period, comfortably outperforming the S & P 500. In

part this is because the company’s 'Equity Investments' have almost tripled to

$76 billion. But earnings per share have declined by 28%. This is due entirely

to a swing on 'Investments and Derivatives' that, by their nature, are highly

volatile. Return on equity has averaged 8% over this period. These are far from

stellar results. The size of the company - net equity is $165 billion - seems

to be a drag on growth. At the current price of $ 152,000 per 'A' share, the

company is valued at 19.4 times estimated 2012 earnings. Is Berkshire

just going through a relatively bad period?

The recently announced Heinz investment will improve earnings

per share; Berkshire will net $1.08 billion pre-tax from the preference

shares and half Heinz's after tax earnings. The funding comes from Berkshire's

float that costs nothing. The deal will enhance earnings by at least 10%.

Berkshire's unsecured debt is rated AA by S&P. Cash and liquid

investments are more than double the company's outstanding debt.

Taking the period 2002-2012, and averaging three year periods at the

beginning and end (and removing non-operating profits and losses), earnings per

share are growing by 15% pa. Equity per share is growing by 12%. Return on

equity has averaged 8%. AA 12-year corporate bonds are yielding 3.9% and I have

added 2% for operating risk and 5% for a profit and margin of safety to arrive

at a discount rate of 10.9%.

This gives an average valuation of $165,000 per 'A' share:

|

Valuation

based on:

|

$

value per 'A' share

|

|

5-year

earnings per share growth to 2017

|

$175,000

|

|

5-year

equity per share growth to 2017

|

$179,000

|

|

5-year

return on equity to 2017

|

$142,000

|

|

Average

|

$165,000

|

|

Current share price

|

$152,000

|

At the current price of $152,000, Berkshire appears to be good

value.

The prudent investor will consider:

1. Will Berkshire's success continue under someone new?

2. Buffett thinks that the insurance float's growth is likely to

tail off. No doubt this is because as the insurance business matures, its

premium growth will slow and its payouts on claims will increase. Given that it

is this float that finances Berkshire's investments for free, this will have a

knock-on effect on earnings.

3. How long can such a large company find good deals that will make

a material difference to earnings? Where will the growth come from?

No comments:

Post a Comment